Japanese Trading Companies (Part 1)

Buffett's first investment in Japan

Note: This article was originally written on February 11, 2023

Despite Berkshire’s investments in the Japanese trading companies more than two years ago, not much has been written about them in the English language media.

Buffett has observed Japan for longer than anybody, but never actually invested in Japanese stocks (in a past interview from 20 years ago, Buffett commented that he liked Sony, but also thought the stock was expensive). So what made him pull the trigger this time? What made these companies so compelling that Buffett decided to make his first investment in Japan, at the age of 90!

In Berkshire Hathaway’s press release (August 31, 2020), Warren Buffett wrote:

“I am delighted to have Berkshire Hathaway participate in the future of Japan and the five companies we have chosen for investment. The five major trading companies have many joint ventures throughout the world and are likely to have more of these partnerships. I hope that in the future there may be opportunities of mutual benefit.”

The author (Daye) started his buyside career as a Japan analyst and has studied these trading companies closely, meeting with the senior managements of trading companies on many occasions over the past ten years. Berkshire’s investment was surprising, but then it makes total sense. The Oracle is always a step ahead. The goal of this report is to help readers put together the pieces of this very fascinating but highly nuanced group of companies.

Introduction

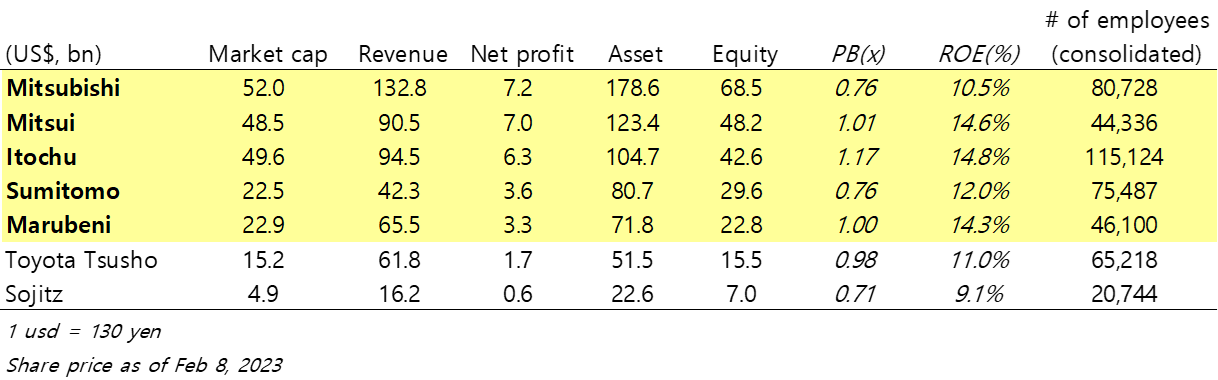

Sogo Shosha means “General (=Sogo) Trading Company (=Shosha)”. The name itself doesn’t carry a lot of meaning but today it specifically refers to seven large-caps: Mitsubishi, Mitsui, Itochu, Sumitomo, Marubeni, Toyota Tsusho, and Sojitz. All are listed on the Tokyo Stock Exchange (and have US-listed ADRs too). In this report we will use the terms “trading company”, “Shosha”, and “Sogo Shosha” interchangeably.

A quick look at the numbers shows that collectively they account for more than US$200bn in market cap and $30bn in net profit. This is not some small obscure industry! The top three (Mitsubishi, Mitsui, Itochu) are somewhat comparable in size. The largest is Mitsubishi, which has market cap of ~$50bn, $7bn in net profit, and employs ~80k employees (across all subsidiaries). Berkshire invested in the five largest Shoshas, which are highlighted below in yellow.

Shoshas are diversified entities that own a large number of business interests both in Japan and globally. They are major players in the metals/mining and energy sectors, and have entered into JVs in iron ore, metallurgical coal, copper, and LNG projects around the world with global majors. But they also have a lot of investments outside of commodities. For example, Mitsui owns 33% stake in IHH Healthcare, the largest hospital group in Asia, and 17% stake in Penske Automotive in North America. Itochu has a 10% stake in China’s CITIC Limited. Family Mart (Japan’s second largest convenience store chain) is owned by Itochu, while the third largest chain Lawson is owned by Mitsubishi. These are shown below. It’s not even a full list, but you get the idea.

They are extremely diversified (often said that they handle everything “from noodles to satellites”) and because of this, investors easily get lost in the diversity of their business operations and fail to grasp the big picture. There is also no “Western comp”, further making them challenging to understand. Interestingly, the rating agency Moody’s recognizes Sogo Shoshas as its own unique category, separate from other conglomerates and distribution businesses.

Now, gun to my head if you asked me for a Western equivalent, I would say there are some similarities to the following:

Berkshire Hathaway - diversified conglomerate that takes stakes in other companies ranging from minority investments to controlling stakes.

Jardine Matheson - diversified conglomerate with roots in commodities trading in Asia

Goldman Sachs – strong talent pool and network across private sector and the government

But to be honest I don’t prefer these analogies because in the end, it’s still apples-to-oranges. To understand Shoshas you need to actually study Shoshas.

So Shoshas haven’t been the most accessible for Western investors to study. But actually, you might be surprised that even many Japanese investors have missed the big picture. First, investors didn’t want the large resources exposure that came with most Shoshas. But more important is that many have not grasped the important transformation which have happened with Shoshas over time. As Shoshas have historically neglected shareholder value, there continues to be skepticism (and granted, some are warranted). But the Shoshas today are not the same as Shoshas twenty years ago, while I would argue that investors’ understanding of them have lagged. One of the key themes in this report is that we will be exploring the transformation of Shoshas in depth.

The Business of Shoshas

At the most general level, Shoshas do three things:

Trading;

Investing; and

Operating the different businesses they have invested in (in the cases where they have acquired a controlling stake).

Let’s look at each in turn.

Trading: You can also call this wholesaling or distribution. Shoshas trade practically everything - you name it, they probably do it. It’s often cross-border. For example, selling Australian iron ore to Japanese steelmakers. Or selling Norwegian salmon to Japanese supermarket chains. Or, they could sell Japanese chemical products to overseas users. As the middleman, Shoshas earn a spread or commission income, typically as percentage of total value of goods distributed. They also engage in adjacent functions like consulting and provision of credit.

The trading business served as the genesis for Shoshas, and it used to comprise the majority of Shosha’s business until around 1980’s to 90’s. But the importance of “trading” was eventually overtaken by “investing” as Shoshas focused on trying to create value through deploying their own capital, rather than just serving as the middleman. In this way, Shoshas became more like investment organizations over time.

Investing: Shoshas invest using their own capital, and investments can range from minority investments (5-10%) to equity method affiliate (20-50%) to controlling stakes (50-100%). The investments are done opportunistically, but a lot of the times they invest in value chains where they have experience operating and have intimate knowledge of.

All of this might sound a bit abstract, so let’s look at two examples to see how these investments are typically structured - one in the retail sector and another one in commodities.

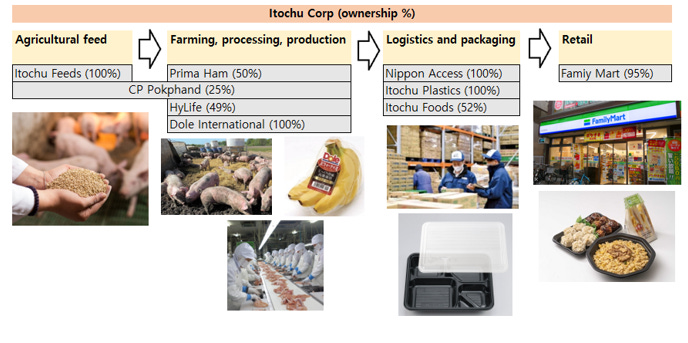

In retail, let’s look at Itochu’s investment in the CVS chain Family Mart, which it acquired via a take-over-bid in 2020. In the diagram below, take note of the fact that Itochu has ownership interests across the value chain. Importantly, Itochu has been doing business extensively with Family Mart even before the TOB. Through its logistics subsidiary Nippon Access, Itochu handled all the delivery (replenishing each Family Mart’s store inventory three times a day) and even designed and manufactured the plastic food containers and packaging for the store’s ready-to-eat items like bento boxes. It has consolidated the value chain for some of the popular items including Family Mart’s famous fried chicken and fresh sandwiches, from animal feed to farming/processing of chicken and livestock to retail sales. By the time Itochu decided to take full control of Family Mart, it already knew the business better than anyone in the world.

In commodities, let’s take a look at Mitsui. It own a 6.4% direct stake in Vale (which alone is worth more than $5bn at market price). In addition, Mitsui has entered into JVs around the world, with individual project stakes ranging from 1.5 to 33% as shown below in iron ore, metallurgical coal, copper, nickel, and LNG. Mitsui and Mitsubishi are the most exposed to commodities out of all the Shoshas, with 50-60% of profit coming metals and energy (compared to Itochu with less than 30% and other players somewhere in between). You can say that investing in Shoshas is one way to gain commodities exposure - a possible alternative to investing in miners and oil companies.

If you are familiar with global commodities trading firms like Trafigura/Glencore, then you can basically think of this being similar except hyper-localized to the Japanese market with respect to their customer base and supply chains.

A very important point is that in the early days, Shoshas saw investing as purely a way to secure distribution rights to resources and goods for its trading business. For example, in return for contributing the capital to develop an iron ore project in Australia, Shoshas obtained the rights to the output of that mine (which they then sold to their Japanese steelmaker customers). At times, the investments may not have had great risk-reward as a standalone deal (and they knew this), but that didn’t stop the Shoshas from making them as long as the distribution rights could be secured. Sometimes it all worked out, other times it didn’t.

Eventually, all of this changed. Investment decisions became detached from trading operations as the importance of their trading operations declined over time. In this sense, Shoshas turned into real capital allocators. For example, Itochu’s acquisition of Family Mart above had nothing to do with securing any distribution rights, and was made purely on the basis of trying to earn an attractive return on capital - just like the goal of any other investment organization.

Operating: Following Itochu’s acquisition of Family Mart, Family Mart became a subsidiary and its results consolidated into Itochu’s financials. In the accounting/technical sense of the term, Itochu is an “operator”. Depending on the specific subsidiary Shoshas can either be very hands-on operators, or they can be passive. In the case of Family Mart, Itochu is quite hands-on given the scale and importance of the deal.

To give a rough mental image of the profit breakdown, in 2022 Itochu generated about 50% of total profits from its investment portfolio (consisting of minority stakes, equity method affiliates, and dividends received), 40% from operations of consolidated subsidiaries (Family Mart and others), and estimated teens percentage (or less) from commission revenue generated from the trading business. Even though Shoshas had their roots in trading, it’s important to recognize that trading no longer is the main contributor to their earnings.

We will come back to all of this with more detail later, but for now, understand the following:

Shoshas are extremely diversified, both 1.) in terms of the industries they operate in, and 2.) ways that they make money (through minority investment stakes, buying out entire companies, making commission revenue from trading, etc.) Shoshas are creative organizations, and there is no single fixed way in which they do things. At the risk of oversimplifying, it’s about a group of smart people, backed by organizational network and capital, looking out for ways to make money in the real economy. When distilled in this way, is it super different from other investment conglomerates around the world? Not really.

The misconception

Many investors have the image of Shoshas being dinosaurs: 150-year old businesses which are past their peak and are remnants of Japan’s rapid post-war industrialization. This is a misconception.

Look no further than the fact that Shoshas still to this day attract the best talent in the country, from all the target schools. Below is one brand survey conducted for the class of 2024. Itochu ranked #1, and two other Shoshas made it to the top 10 list (Mitsubishi Corp and Marubeni). They were ranked even higher than Sony, Toyota, and all other Japanese blue-chips. Usually, no matter what survey you look at Itochu comes up in the top 3, and other Shoshas come in highly too. Shoshas are a force to be reckoned with in Japan’s hiring market.

Shoshas also consistently rank the highest in Japan for compensation rankings. Below, four Shoshas made it to the top ten salaries list. Mitsubishi Corp paid the highest at 16.8 million yen per year. The average salary in Japan is in the 4-5m yen range so Shoshas pay 3-4x higher than the country average.

As an aside, if you asked smart and ambitious Japanese college graduates why they want to work at a Shosha, the answers are usually high pay and the opportunity to be “thrown in” from a young age. Shoshas are known for giving their younger employees hands-on experiences and responsibilities. This is attractive especially in a seniority-obsessed workforce like Japan, where it’s not uncommon for even 40 year olds to be considered “relatively junior” by some companies’ standards!

Berkshire’s investment

Shoshas were Berkshire’s first investments in Japan. Berkshire started buying five of the largest Shoshas in August 2020, accumulating ~5% stake in each of them, and also filed for the potential to acquire up to a maximum of 9.9% in each. Then in November 2022, Berkshire added to each (roughly 1%). The fact that Berkshire still has quite a lot of room to increase its stakes (before getting to the 9.9% threshold) is acting as a strong valuation support for the sector.

Buffett hasn’t commented much about his investment in Shoshas, so as Buffett watchers the best we can do is come up with our own educated guesses. There are several thinking points:

Inflation hedge: Around the time of the initial purchase was when Buffett had been publicly expressing his inflation concerns. Shoshas are inflation-protected. They own substantial stakes in mining and energy interests globally, and also have stakes in places like agriculture and food where prices are going up. Their trading businesses earn a commission on total value of goods and is inflation protected.

Basket approach: The CEOs of Itochu and Mitsubishi were interviewed, and they both said Berkshire’s investment came out of the blue. They were surprised, but showed an upbeat and welcoming stance to Berkshire’s investment. If I had to guess, it seems unlikely that Berkshire had a lot of deep interactions with the management beforehand. Supporting this is the fact that Berkshire took a basket approach, which deviates from what I would expect Buffett to do generally which is to buy more concentrated stakes in a smaller number of firms with more conviction (for example, look at Buffett buying large stake in OXY as opposed to, say, investing smaller stakes in every large shale producer).

Carry: Investment amount (625 bn yen or about US$5 bn) at the time was funded by yen debt with very low interest rate. Trading companies were yielding 2.4-5.4% in dividend, so the carry was attractive.

We offer three predictions here:

1.) It looks like Berkshire’s initial purchase of Shoshas was more quantitatively driven (inflation protection, cheapness), and more reflective of Buffett’s style in the 60’s and 70’s. But over time Berkshire may focus more on the qualitative aspects including management and capital allocation. Indeed, we believe that it is the latter that is the most interesting with these firms today. After all, everyone can calculate NAV, but reading into capital allocation is where there is real opportunity to identify value creation. In essence, “buy for the inflation protection and cheapness, but stay for the improvement in capital allocation”. In the future, I think there is possibility for Berkshire to selectively boost stakes in Shoshas with the best management teams, rather than buying them all equally. And as we’ll discuss later, there is indeed a pretty big gap in the quality of management and their capital allocations among the five Shoshas.

2.) A bigger picture prediction is Berkshire’s involvement with these companies may be a prelude to them becoming more active in Japan in the future. Perhaps Berkshire gets introduced to co-investment opportunities in Japan. Notice that in Berkshire’s news release, Buffett says he is participating “in the future of Japan”. For anyone that invests in the Japanese market, this is potentially a very exciting story. If Berkshire started investing more in Japan, surely global investors will follow.

The following comment from the CEO of Mitsubishi is interesting:

“Perhaps Mr. Buffett wanted to have discussions or debates about other companies in Japan if there was some kind of opportunity. For foreign investors, trading companies are a gateway to Japan. Trading companies have business dealings with pretty much all industries and it’s a quick and efficient way to tap into the Japanese industry”

- Kakiuchi Masahiko, CEO of Mitsubishi Corp

3.) This is not so much a prediction like the first two, but Berkshire’s involvement might also motivate the senior management of the trading companies to explore capital allocation at a deeper level. It’s not guaranteed that this will happen, but it’s interesting to think about - will we ever see a CEO of a Japanese trading company attend a Berkshire annual meeting?

“We are upbeat about the fact that the most respected investor in the world has purchased our stock. There is fear that Japan is being increasingly isolated from the rest of the world, but the fact that Mr. Buffett has chose to invest has given us stimulation and takes us in the right direction”

-Okafuji Masahiro, Chairman and CEO of Itochu

Understanding Shoshas at a deeper level

To invest in Shoshas, you have to understand their history. Specifically, it’s important to understand Shoshas and their development in the context of Japan’s Keiretsu. In Section I below, we dive into the history of Shoshas. Section II will take us back to the business model of Shoshas, where we will examine their trading and investing operations in more depth. Finally, Section III will look at the transformation of Shoshas’ earnings base.

This is where the pieces will start to fit together, and by the end you will be able to develop a good mental model of the workings of a Japanese trading company.

Section I: History

Pre-WWII

Trading companies first came into existence in the mid-1800’s, after Japan re-opened its ports to trading with the outside world (after being closed off for over 260 years under the isolationist policy of the Tokugawa Shogunate).

Powerful family-run conglomerates (called Zaibatsu) came to power and operated the trading businesses with foreigners. Mitsui and Mitsubishi were the earliest such Zaibatsu. Zaibatsu is a term you might have heard, and it has strong connotation to monopolies. In fact, that’s what they were until the end of the second world war when Japan’s anti-monopoly laws came into force in 1947.

Japan possessed little natural resources of its own. Japan imported raw materials from overseas, added value through manufacturing, and then exported the finished products. Trading companies took advantage of the business opportunities created in this model. Textiles were the first major business. Trading companies would import advanced equipment and machinery from the UK and Germany, and cotton and raw materials from India. They then sold these to the nascent domestic textile industry (also provided the industry with funding support and technical training). Once the manufacturing was done, trading companies then took these products and helped find markets for them overseas.

In addition to the textile business, trading companies had other businesses too like shipping and the importing of commodities and food. These were successful, making trading companies powerful and rich, and allowed them to grow to even bigger size by expanding into banking and insurance in the early 20’s century. Their power became unchecked as they grew to dominate the whole economy. Trading companies had close ties with the government and corruption was also rampant. They enjoyed a cozy relationship with Japan’s wartime government and supplied Japan’s war efforts both in the conquest of Asia and in WWII.

After Japan’s defeat in WWII, GHQ (General MacArthur) ordered Zaibatsus to be dissolved due to their close ties with Japan’s military government and because they were monopolies. Mitsui and Mitsubishi were broken into hundreds of entities, separating out the trading business from banking, insurance, and the various manufacturing operations. This was the big bang that gave way to the industry structure as we currently know of today.

Keiretsu

Although Zaibatsus were dissolved, these entities still maintained loose ties and evolved into loosely organized alliances known as the Keiretsu.

Within a Keiretsu (such as Mitsubishi), companies held each other’s stocks to deepen their alliance. This is known as cross-shareholdings.

A typical Keiretsu consisted of 1) a group bank, 2) a group trading company, 3) one or more group insurance companies, and 4) a large number of group manufacturers/operating companies. The group bank and the trading company sat at the center and did business with everyone.

The bank and trading company co-existed and enjoyed a symbiotic relationship. Typically, the bank took on the role of making loans for large capex projects, while trading companies funded the working capital of customers. The funding needs of SMEs typically relied much more on the trading companies, as banks didn’t want to take on the credit risk of smaller companies. By being on the ground and dealing with customers in their day-to-day operations, trading companies had a much better grasp of credit conditions in the SME space than the banks did.

There used to be six major Keiretsus - Mitsui, Mitsubishi, Sumitomo, Fuyo, Sanwa, and DKB Group (Marubeni belonged to Fuyo, and Itochu to DKB). Over time, through reorganizations and M&As some of the groups got broken up, and today only the first three still exists under the original name.

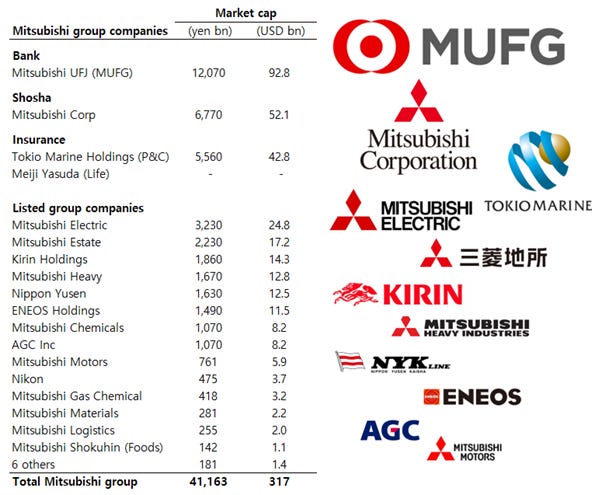

Below, let’s take a look at Mitsubishi, which is considered the most powerful and prolific Keiretsu. Take note that Mitsubishi Corp (the trading company) has the second largest market cap in the group, after the main bank MUFG. Another interesting point is that not all members carry the name Mitsubishi e.g. the beer company Kirin and the camera maker Nikon.

One question that gets asked a lot is why Shoshas are so diversified. The Keiretsu structure offers one explanation - the trading company dealt with all group manufacturing and operating companies. Keiretsu is also a reason which prevented “specialized” trading companies (Senmon Shosha) from becoming more dominant in Japan, as the Keiretsu kept dealings inside their own groups and locked outsiders out. While all kinds of specialized trading companies exist in Japan (focused on a specific niche, like food), to this day they don’t have the scale nor prestige that the generalized trading companies command, and are disadvantaged in the hiring market.

Keiretsu provided a model for Japan’s post-war growth. The advantage is that it allowed for faster information sharing and coordination within the group. Sometimes it was very powerful when all members worked towards a common goal in unison. The drawback and criticism of this model is that it breeds insularity and complacency within the group, in addition to being bad on corporate governance. For minority shareholders this was a common problem. At times, Shoshas acted as a purse for the Keiretsu (expected to “take one for the team”), investing in projects that would advance the group’s collective interests but were questionable in terms of the merits for its own minority shareholders.

Fortunately, these governance issues are less of a problem today, as the Keiretsu has been relegated to more of a legacy structure rather than the way businesses are still conducted in Japan. Cross-shareholdings have also been significantly reduced. Corporate Governance has been the core subject of reform, and there has been real progress. Nonetheless, it’s still important to understand the path which Shoshas took to get to where they are today, as Keiretsu was absolutely the defining feature of how business was done in Japan during its four or five decades of rapid post-war growth.

Post WWII

Shoshas rode the wave of Japan’s rapid industrialization by expanding the model it used in the textile trade, as discussed earlier, to other growth industries including steel, chemical products, and other manufactured goods, and became diversified trading houses. It is said that at the peak, over 50% of Japan’s exports and 75% of the country’s imports went through one of the major Shoshas.

Some of the growth came by M&As - for example a textile focused Shosha acquiring another Shosha that focused on steel. The 1950’s marked a period of significant consolidation, and by the 1960’s the industry had consolidated to about 10 major Shoshas.

During the oil shock of the 1970’s, Shoshas cultivated a new business of building petrochemical refineries in the Middle East (“plant exporting”). These were massive projects which required high-level project risk management. As the organizer, Shoshas brought together the fragmented Japanese industrial base and provided a one-stop solution to foreign governments and SOEs. This is one example where the Keiretsu structure provided value, as information sharing and coordination within the group helped Shoshas to generally deliver these mega projects on time and on budget. It was an attempt by Shoshas to add value in its own unique way, while also allowing them to secure the distribution rights to more products after the completion of the refineries.

However, in the 1980’s, hardship would arrive for Shoshas (in what would be referred to as the “Shosha winter” period). Shoshas saw their growth slow down and in some cases started losing businesses. Several big things hit Shoshas during this period:

One of the problems was that as Japan’s growth engine shifted from textile/steel/chemicals to consumer electronic/automobile, new winners started to emerge like Toyota and Sony. These companies pursued a strategy to be closer to consumers, and wanted to more directly manage their own sales network. By virtue of their scale, these firms also had the capital and human resources to do a lot more things in-house, eliminating the middleman. This gave way to a wave of disintermediation which hit the Shoshas.

Another blow was the massive strengthening of yen following The Plaza Accord (1985) which hit Japan’s export industry hard. Indirectly, Shoshas were also hit. Finally, when Japan’s bubble burst (1991), this was like the final nail in the coffin. Shoshas recorded massive losses due to bad loans and their speculative investments in real estate and other financial assets. By then, people thought Shoshas were going to be gone.

However, eventually Shoshas proved the doubters wrong by transforming themselves over the next 20 years. However, what it took was a near-death experience post the bursting of Japan’s bubble.

Before we end Part 1 of this deep dive, we need to answer one important question: How did generalized trading companies become so big only in Japan, and why is this a Japan phenomenon? There have been lots of discussions of this in the Japanese academia and literature. For example, renowned Shosha expert Takayuki Tanaka examined the history of trading companies in other parts of the world:

He observes that in the past, there were a large number of general trading companies in the UK and Germany too. But they mostly ended up either being disintermediated and going out of business, or were forced by shareholders to divest their portfolio assets, becoming more niche and smaller over time.

In Korea (which is most similar to Japan), there were trading houses which existed as part of larger powerful conglomerates (Chaebols) like Samsung, LG, and Hyundai. However, in these places the power (and family wealth) were typically concentrated in the manufacturing companies, and the trading houses were simply relegated to the role of being a sidekick or just a “contact center” for the group. Also, unlike Shoshas the Korean trading houses also dealt far less in imports than they did with exports.

So what had allowed conditions to be so ripe in Japan for Shoshas to dominate? There were three key factors in our view:

1. Insularity and cultural uniqueness of Japan

Shoshas served as the bridge between the outside world and Japan. They were heavily relied on to do business overseas. For example, during Japan’s rapid industrialization period many Japanese manufacturers simply tasked Shoshas to help find markets for their products overseas, instead of hiring and training their own dedicated overseas salespersons. They could simply sell their products to Shoshas without putting efforts themselves to learn English or interact with foreigners.

In fact, our hypothesis is that Shoshas are actually partly to blame for making Japanese businesses even more insular than they already are. It’s a chicken-egg problem but to this day, doing business overseas and dealing with foreigners is not a strong suit of most Japanese businesses.

2. Japan’s relatively fragmented business landscape

Simply, if one company came to dominate everything in an industry, then the middleman will lose power and be disintermediated. In Japan, many industries continue to be quite fragmented. Even after large companies like Toyota and Sony emerged, Japan still hasn’t lost its SME base.

3. Keiretsu

Being part of their Keiretsu alliances helped Shoshas ride the strong growth of post-war economic boom, alongside their group manufacturing companies which were the main direct beneficiaries.

Keiretsu members paid respect not to disrupt each other’s domain. For example, in Germany, large automakers brought import/export functions in-house and disintermediated their trading firm partners. But in Japan, Mitsubishi Motors continued to do business with Mitsubishi Corp.

To varying degrees the above factors are less relevant today, as the Keiretsu structure has lessened in its influence, and as technologies like the internet has brought down the barriers to doing international business and reduced the massive informational advantages that Shoshas once wielded over their customers. But these still explains the historical reasons why Japan provided such a ripe environment for trading companies to flourish and allowed them to reach the scale that they have today.

~END OF PART 1~

We continue our discussion in Part 2, where we delve further into the role of Shoshas as investment entities, and also compare the five Shoshas that Buffett has invested in examining their business portfolio, management, and capital allocation.