Japanese Trading Companies (Part 2)

Closer look at the business model, management, and capital allocation

Note: This article was originally written on February 27, 2023

Welcome back! This is Part 2 of our deep dive on the Japanese trading companies. Building on the content from Part 1, we explore the business model and the transformation of Shosha in greater detail. We also compare the five major players that Berkshire has invested, giving particular attention to evaluating management quality and capital allocation.

In Part 1, we introduced two major business activities of Shosha: trading and investing. Let’s start by revisiting these, with an emphasis on understanding the competitive advantages that they have in each.

Trading

In Part 1, we discussed the “Shosha winter” period of the 1980’s, where disintermediation was one of the troubles to hit the trading companies. Since then, the threat of disintermediation has always been present. But what’s also true is that disintermediation has played out over four decades, having largely run its course, leaving the trading companies today with entrenched businesses that have generally proved to be stickier and harder to disintermediate. One such business is resources and energy, which we examine below.

Trading companies utilize a mixture of midstream assets that they own in-house or contract from third-party. These include storage and blending facilities, terminals, ships and barges, trucks and rail freight, and light processing facilities. Demand patterns for commodities can be uneven, especially for metals, requiring trading companies to respond dynamically to customer demand. While holding inventory, commodity price fluctuates which means market risks have to be managed or hedged. Trading firms also have operations to blend oil and minerals from different sources in order to meet the quality requirements of each individual customer. All of this is to say that the operational complexity and capital requirements of moving certain goods can be fairly high.

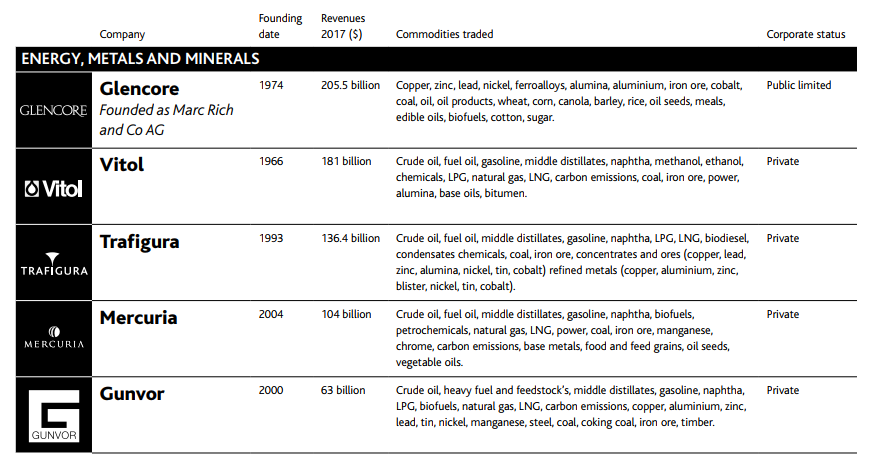

The global commodities trading industry is quite fragmented, with the largest global players listed on the chart above. Relative to these global players, where the Shoshas are really strong is in their relationship with the Japanese buyers. They move large volumes in Japan, and are able to provide better service to Japanese buyers with assets and supply chain that are optimized to serving a single geography. For example, they are highly flexible and responsive to meet the very precise delivery schedules of Japanese manufacturers. Another advantage of Shoshas is their access to low-cost borrowings through strong relationships with their Keiretsu banks. This is often passed down to customers in the form of favorable credit terms - extended payment terms or lower rates than what the customers could obtain on their own. Shoshas also cross-sell more products and services with their Japanese clients, and tend to have wide dealings. For all these reasons they have a very solid business foundation in Japan that outsiders have had a hard time breaking into.

More importantly Shoshas own joint venture interests in mines and oil/gasfields around the world, and thus cannot be disintermediated because they own the actual supply. And with China dominating the global demand picture across most commodities, Japanese demand is increasingly seen as a valuable hedge for many of its partners - especially commodity-producing Western nations like Australia. On this point, it’s also worth noting that Shoshas have the backings of the Japanese government, and will continue to have a seat at the most important resources and energy projects of its allies and partners around the world.

Another reason that Shoshas can’t be disintermediated easily is because they deal with lots of SMEs and not just big customers. Due to capital constraints smaller customers don’t have the resources to build out their own direct sale network, and will continue to rely on the trading companies for distribution. Finally, Shoshas have businesses where they add value through their project management functions and organizational capability of bringing together many suppliers, which makes them harder to disintermediate. An example of this is urban development. But enough on this topic - what’s interesting about Shoshas today isn’t their trading operations. Much more important is their capital allocation, and this brings us to the next area: investing.

Investing