$ATAT 101 - Atour Lifestyle Holdings

Category leading hotel franchisor for <15 P/E

I am thrilled to collaborate with one of my favorite China analysts, Moatless Capital, in putting together this piece on Atour. Moatless has just launched his new substack, Moatless Musings — make sure to subscribe!

My goal is to produce and curate the best content for investing in East Asia. By collaborating with other talented analysts/investors from time to time, I aim to bring a broader range of ideas and insights for my readers. If you’re interested in a collaboration, please reach out at ddeng@eastasiastocks.com.

Now onto our content!

TL/DR

How would you like to buy the leading upper mid-scale hotel company in China, growing at >30% earnings, for <15x P/E? Intrigued? Read below.

What is an Atour?

(…to shamelessly borrow from Robin Zhu over at Bernstein in his insightful series on PDD)

Atour (“the Company”, “ATAT”, “Yaduo”) is the largest upper-midscale ‘manachised’ hotel operator in China. As at 1Q24, the Company boasted 1,302 hotels (~148k rooms) in operation in China, with 97% of total rooms under the capital-light manachised model. Under this model, Atour is only responsible for sending the Hotel Manager and the “Commissar” (Before we scare you, the role really is that of an ‘HR Manager’ responsible for hiring staff - Chinese companies in general have a tendency to use terminology from warfare - partly because everyone in that generation grew up watching the same war movies, but also because business competition in China is *frequently* war-like in intensity).

Atour collects a capital-light stream of royalties from its franchisees, provides supply chain services, and sells retail products. In turn, the franchisee is responsible for CapEx + location (lease or owned building) and the costs of hotel staff. The Hotel Manager +“Commissar” are also paid for by the franchisee (they are technically on the payroll of Atour, but Atour is reimbursed by franchisees via “monthly hotel managers’ fee”).

Founded by Wang Haijun (who was a veteran of H-World, another one of China’s listed hotel operators - story for another day), Atour positions itself as a ‘lifestyle’ company and aims to focus on serving the ~100mln people in China who have a strong preference for superior service. True to its identity, the company also operates a successful retail business selling private label bedding products - pillows, duvets, blankets, you name it.

In the past, Chinese hotel brands were often perceived as cheap and poorly equipped, with low prices being their only advantage. Today, the landscape has changed significantly. Ask Chinese travelers, and many will tell you that Atour's hotels are at least on par with, and in some areas, surpass foreign brands in service quality and comfort. They have achieved very high customer experience scores and fostered customer loyalty. At the core of this transformation are a strong culture and highly effective management and execution, which we will explore in depth.

In its recent 1Q24 results, Atour grew operating earnings by 60% and the stock trades at ~15x P/E.

Why does the opportunity exist?

The company is virtually locked in on its 2,000 hotels by 2025 target — why is it so ‘cheap’?

Chinese ADRs in general are ‘on sale’ - BABA is 5x EBIT, VIPS was a net/net, etc.

As a result of the RevPar increase experienced in 2023, domestic investors are extremely concerned about short-term negative YoY comps on RevPar driven by lower ADRs (OCC has remained stable) through the rest of 2024 as 2023 was a ‘high base’ year - as management has been cautious about RevPar guidance in the current year. But our hypothesis is really about how the company executes through 2025 and beyond.

H-World is the bigger and more ‘blue chip’ name in the sector - there is a “why not own H-World” dynamic among ADR investors. However, as we’ll demonstrate below, Atour is a ‘different bet’ than H-World.

Liquidity on Atour remains lower - but this past week Legend Capital (PE investor) announced the sale of its next tranche of ~10mln ADRs (~7.3% outstanding), so this is incrementally less of an issue.

China’s Hotel Industry

We believe China’s hotel industry development can be understood in four phases.

Early development and market bifurcation (1980-2000): In the pre-reform era (before 1978), China’s hospitality industry was basically non-existent, with limited options primarily serving government officials and foreign diplomats. State-owned guesthouses were the primary form of accommodation.

With new policies aimed at developing tourism and deregulating foreign capital, the 1980s saw the beginning of China's hotel industry. A bifurcated hotel industry was created.

Foreign capital focused on the full-service upper and luxury segments, with major international hotel groups making early entries into China — Sheraton in 1985, Hilton in 1988, Marriott in 1997, and Hyatt in 1999, among others.

Meanwhile, Chinese players concentrated on the low-end market (Brands such as Jinjiang, Home Inn, 7 Days Inn, and Motel 168 led this sector).

Rapid development phase (2000-2010): The hotel industry entered rapid growth phase thanks to a combination of high income growth and infrastructure buildout. The government invested heavily into the expansion of highways, high-speed rail, and airports, which facilitated domestic and international travel. Events like the 2008 Beijing Olympics and 2010 Shanghai Expo also boosted demand for accommodations.

During this time, Chinese hotel brands focused on expanding their network scale. But the emphasis was on quantity over quality, leading to poor service quality and issues in maintaining standards.

Additionally, as land prices appreciated rapidly during this phase, real estate developers and SOEs built hotels (operating as franchisees of multinational hotel chains) to 'own’ the land and benefit from the real estate appreciation. Frequent travellers in China will note the significantly more luxurious/over-the-top decoration/room size of 5-star hotels - simply because the operators did not intend to make significant money from hotel operations.

Emergence of mid/upper-midscale segments (2010-2020)

The market began to further segment under the efforts of players like Huazhu (H-World) and Atour, which pioneered the middle and upper-midscale segments, becoming the fastest-growing segment. Huazhu entered with the launch of Ji Hotel in 2010, followed by Atour in 2013. Huazhu also acquired another mid/upper-midscale brand, Orange, in 2017.

With rising incomes and a more discerning middle class, previous offerings didn’t meet market needs. Huazhu focused on a clean, affordable, and efficient product offering whereas Atour was more focused on service quality and redefined the experience of staying at domestic hotels. This operating model also made it easier for franchisees to operate.

China’s hotel industry is generally classified into five tiers: economy, midscale, upper-midscale, upper, and luxury.

So, what does an “upper-midscale” hotel look like? To give you an idea, here are some pictures from Daye’s recent trip to China, where he stayed at several Atour hotels.

The following pictures were taken of the common areas and rooms at a regular Atour hotel, which is priced at approximately 450 RMB (~US$60) per night. Prices can be as cheap as 300-400 RMB in some Tier-2 cities or during off season.

The following are from Atour S, which is one level higher than the regular Atour and classified as upscale. It’s priced at ~620rmb per night (or US$85).

Post-Covid (2020~present): One of the key drivers of the industry in the past 5 years is the rapid pace of consolidation among Chinese hotel operators.

Consolidation had already been underway in prior years, including Huazhu’s acquisition of Orange in 2017 and the "Great Consolidation of 2015," which saw Jinjiang acquire 7Days and Home Inn merge into BTG, effectively bringing two major private enterprises into two major state-owned hotel groups.

During COVID, industry-wide room capacity was reduced by 19% from 2019 to 2022, further accelerating consolidation. A significant number of independent operators were wiped out, as without a central reservation system, foot traffic—which used to be a major source of customers—functionally disappeared during rolling COVID lockdowns. This near-death experience elevated the importance (from a franchisee perspective) of being associated with a chain operator - you needed to be in the franchisee WeChat groups to get a sense of how dire the situation was during Covid (and this was the chained hotel franchisees).

What makes Atour unique?

Manachised model

Under the manachised model, franchisees are responsible for the Capex + hotel lease, but Atour appoints and trains hotel managers and onsite HR representatives, allowing Atour to better uphold and maintain service standards across locations.

Franchise agreements are 8-15 years. Atour charge an upfront franchise fee at 4,000-6,000 RMB per room, and monthly franchise fee of 5-6% of gross revenue (think of this as a royalty). The % rate is higher when RevPar is lower, while the % rate is lower when RevPar is higher - the idea here being RevPar is indicative of customers’ willingness to pay - and higher WTP is a function of superior service, and is rewarded. In addition, franchisees must also pay a monthly fixed hotel managers’ fee, fees for using the Central Reservation System (direct traffic), and fees for purchase of hotel supplies.

Atour has a higher exposure towards the manachised model than competitors (excluding retail revenue, 80% of revenue at Atour in 2023 came from manachised model vs. 35% for H-World, 49% for Jinjiang, and 25% for BTG).

This has resulted in more capital light operations and more stable margins throughout cycle for hotels.

CapEx & Payback

The CapEx per Room for Atour properties is approximately 140k RMB, which is about 20% higher than that of a Ji Hotel (H-World). However, the payback is similar at 3-5 years. The higher initial investment is offset by higher RevPar of Atour vs. Ji Hotel. Specifically, the payback of Atour is slightly longer than it is with Ji, but the IRR is similar given higher earnings in the outer years in an Atour.

After 5-7 years, there is an expected “Mid-Life Upgrade” (“MLU”) for rooms that costs ~10-15k/room. Having stayed at Atour hotels of all age cohorts, some of the older hotels have seen wear and tear - while not unacceptable, they would benefit from a refresher. The MLU generally has a payback of ~3 years in the form of higher RevPar than otherwise.

Who are franchisees?

The company’s franchisee selection process is quite stringent - franchisees are generally experienced hotel operators (either independent, or from other hotel chains) with an aligned focus on service. Franchisees are also not allowed to open a new Atour until their existing Atour property hit the target returns. In general, there is a high rejection rate for Franchisees proposing to open new Atour properties - approximately 50% of new hotels are opened by existing franchisees and 50% are from external experienced hotel franchisees.

Customer loyalty

Atour boasts very high customer review score on Ctrip (~4.8/5), and as of 1Q24 enjoys over 74 million A-Card loyalty members.

Most of Atour’s loyal customers are young. According the company, 70% of customers are under 40 (but in reality this should be even higher as we believe a large number of older guests staying at the hotel belong in the category of “accompanying grandparents”)

Customer loyalty is reflected by the fact that CRS (Central Reservation System) Revenues represented ~2/3 of total revenues — this represents direct booking made through Atour’s app/mini-program and corporate customers, which helps reduce the brand’s reliance on OTAs. Additionally, there are anywhere from 10-15% of ‘walk-in’ customers off the street, so total ‘direct’ traffic is ~80%+. Similar to the Marriott Bonvoy and Hilton Honors of the world, Atour (and H-World) are implementing “points only if you book direct” programs to drive higher direct traffic. OTAs will likely remain relevant as a good ‘new customer acquisition channel’ and it will be on the hotels to ‘keep them’.

Atour offers a complete and seamless digital experience through its app — customers can customize their room preferences prior to check in, contact staff and lodge complaints during stay, and check out after stay.

Productization of service

Atour borrowed the tech company playbook of “productizing” services. They have 40-50 kinds of these service products based on 17 touchpoints that have been identified with customers (e.g. when customers make a booking, when they check in, during the their stay, when they check out, etc.)

Here are some examples (Let us know how many of these you can find at a Marriott property).

“Hangover Honey”

One of the most impressive ‘products’ that Atour offers is the overnight tea. Frequently, business travelers in China have to engage in entertainment as part of business banqueting. Within these meetings, baijiu (more on baiju to come in future posts) is often a mandatory part. What Atour offers is a specialized blend of tea with honey that they will leave on the bedside table for travelers, along with a Thermos of hot (but not scalding) water - for said traveler to drink when they stumble back to the hotel.

“Yaduo Tea”

In the hotel rooms, you will find bottles of Atour branded teas - from the Yaduo village in Yunnan province. Due to popular request, the company has made this available on its E-commerce platform (within the Atour App) for ~4 RMB/bottle (pro tip: we recommend the sugarless Green Tea).

Yoga mats

Guests can request yoga equipment in the room. Popular among female guests who want to get a morning yoga session in but doesn’t want to visit the gym in the morning (no need to get dressed, do hair, etc.) This can be done by using the Atour app prior to checking into the hotel.

Free night time snacks

Hotels serve free buffet style noodles/dumplings/congee and other Chinese style light appetizers from 9-11pm. These are highly appreciated by guests checking in late (especially for those who are semi-inebriated after a business banquet - those of you who’ve eaten noodle soup after drunken karaoke - you know what we’re talking about) as most restaurants are closed at this time.

Takeout breakfast

For guests who are busy in the morning to rush to catch their flight, train, etc. they can request for packaged breakfast to take on the go when checking out.

Disposable socks & undergarments

For the unfortunate business traveler who was unable to pack before being sent on an overnight business trip (not an uncommon practice in China).

Retail Business

Huh? Retail business? Isn’t this a hotel? Atour has a retail sales area on the lobby where customers can purchase Atour’s private-label products (these are also available for sale through e-commerce).

Sleep products are most popular (pillow, blanket cover, etc.) but also for sale are personal care items (shampoo, toothpaste, handwash etc.), food items (the famous Atour tea, biscuits and cookies), light appliances and more.

Atour’s GMV grew 277% in 1Q24 to RMB495 million. (The company had targeted 450mln of Revenues for FY2023 in April 2023, but they generated 970mln). On one hand, it shows how the company has been extremely successful in the Retail business; but on the other hand it also shows how this business is harder to handicap in terms of upside. Further success relies on the company’s team executing - figuring out the exact preferences of customers and identifying the correct product market fit. The company has discussed targeting Retail business to be equal to the revenue of the Hotel Business.

Below are pictures of the retail sales areas:

Culture and management

“让人与人之间有温度地连接 ” (To warmly connect people together)

- Mission Statement of Atour

In the end, there is nothing “proprietary” about any services business. Anyone can copy any single aspect of Atour’s services, like the “Hangover Honey”. However, what can’t be easily replicated is the culture, which is truly the secret sauce. This is what really separates Atour from the rest.

This is an appropriate time to bring up the meaning behind Atour (亚朵 or “Yaduo” in Chinese). Yaduo is a small village in Yunnan province. Founder Wang Haijun was inspired by their hospitality and way of life after visiting the village. He dedicated the company’s culture to emulate what he saw there, and Atour’s employees are trained to treat guests like villagers in the Yaduo village (the company also arranges corporate outings for employees to experience Yaduo village).

For example, one of the first things guests would notice upon arrival at the hotel is that, instead of wearing suits and ties employees wear Atour T-shirts. This helps foster a sense of a campus or community-like feel.

Atour’s employees are usually young (mostly 20’s and 30’s), friendly, with a “can-do” attitude.

One of the major problems with China’s services industry in the past has been overly rigid service, where employees only knew how to do things by the book. There was fear of getting into trouble, which led to highly inflexible services.

Atour, on the other hand, delegates authority to front-desk employees, empowering them to help customers solve various problems, even unforeseen ones. For example:

“Each of our hotel staff is granted a budget each month that they may utilize in their discretion to help the guests with their unique needs, be it buying medicine for the guests or accompanying them to the hospital”

- Atour 20-F

The company is also obsessed with responding to customer feedback and complaints.

They have a policy that each hotel must resolve customer complaints on the same day. The hotel industry norm is to hold weekly meetings to address complaints (leaving customers likely to hear back only after their stay, which is too late), but at Atour complaints cannot be left overnight.

“As part of the Atour SOPs, our customer experience department collects all the complaints left in the past 24 hours from our booking channels as well as social media platforms, compiles and sends them to each responsible hotel manager before 12 p.m. each day. Hotel managers are required to follow up with the guests who left the complaints within the next five hours, learn from them the potential areas for improvement, and submit a rectification plan addressing those issues for approval by our customer experience department. If the rectification plan is not approved, the responsible hotel managers are required to discuss, analyze and propose new plans in a dedicated Weixin/WeChat group.”

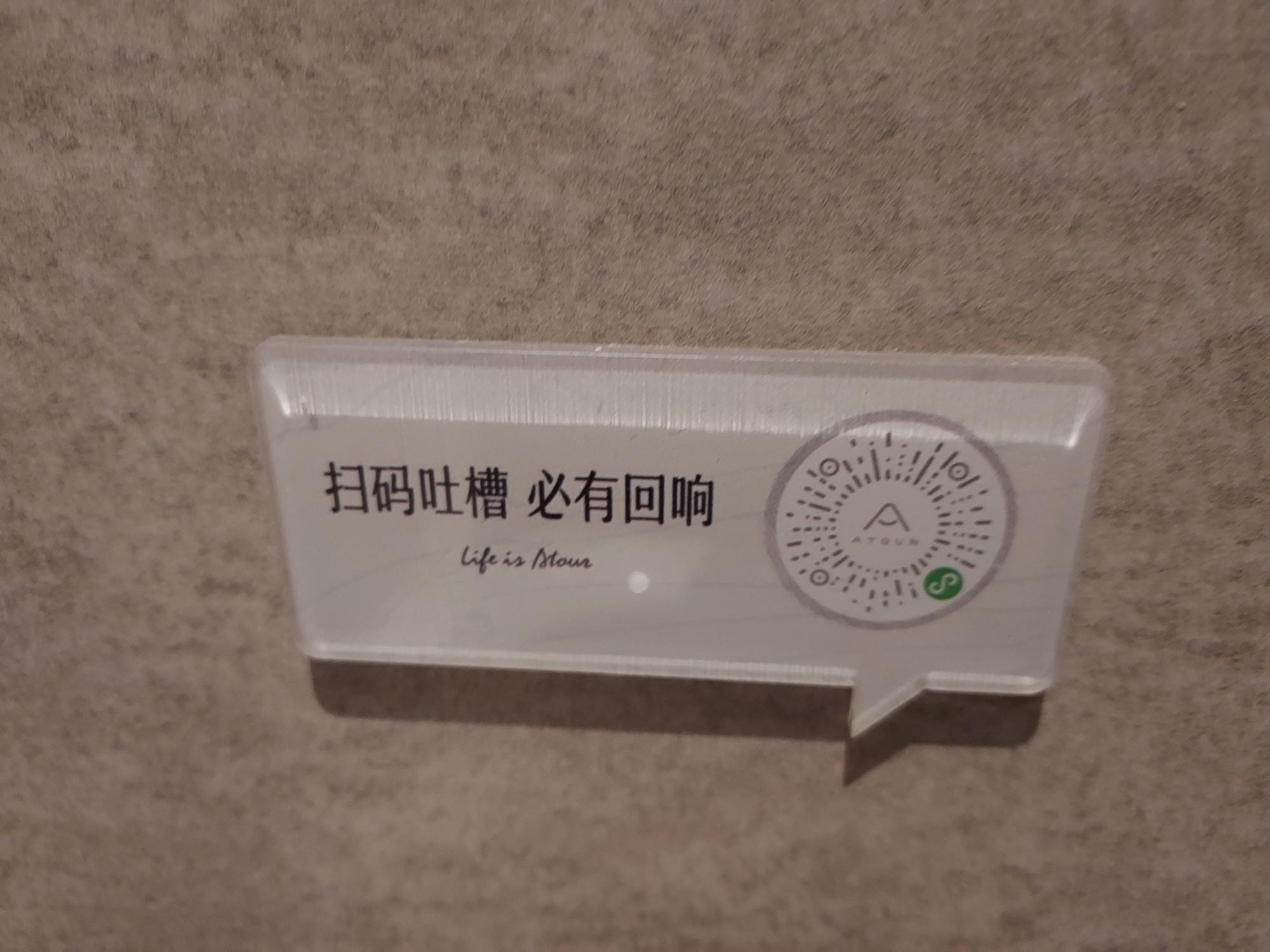

When staying at Atour, guests can see little signs in their guestrooms that say 扫码吐槽 必有回响, which translates into “Scan the QR code to give feedback/complain, and we will definitely respond." Not many hotel chains actively encourage customers to complain!

Here’s a memorable experience from Daye’s recent stay. A front desk staff offered me a free breakfast in exchange for helping them write a review on Trip.com. I agreed, but forgot to write the review (to be honest I was too lazy and had no intention to do so). Later that day, when I walked past the front desk, the same staff was waiting for me and handed me a gift bag filled with snacks, likely purchased at the convenience store next door and asked once more for my review. I usually don’t write reviews, but I relented this one time.

The fact that competitors are getting outhustled does not surprise me at all. This is the element of Atour that is vastly differentiated vs. H-World in both customer experience, corporate strategy, and investment thesis. While H-World has openly touted its goal of entering the upper mid-scale hotel category, they have a ‘too many cooks in the kitchen’ problem - none of their upper mid-scale brands - Crystal Orange, Orange, Mercure, Joya - are at a sufficient scale - and are all competing internally for resources - leading to subpar execution.

Wang Haijun

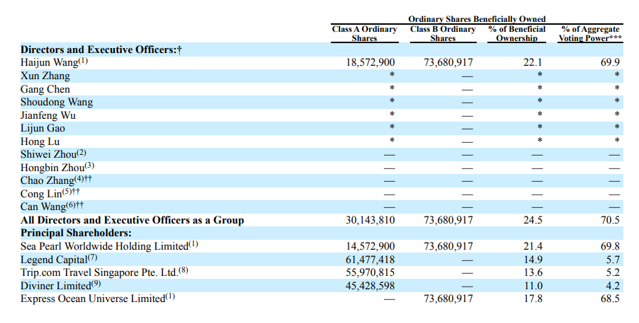

Founder Wang Haijun owns 22% of the shares, but 70% of voting power due to dual class structure. Wang used to be an EVP at Huazhu (H-World), and he also has experience at Home Inn, Jinjiang, and Ctrip.

Note that Atour does not employ a VIE structure. Offshore investors of ATAT have direct ownership stakes in the onshore companies, as shown below.

Upgrading? Downgrading?

By now we’ve hopefully offered a thorough review of Atour’s value proposition to both customers and franchisees. It is important to understand the context of Atour and its various customer groups. Reading about Chinese Consumers in mainstream media cannot be done without seeing words like 'tepid', 'weak', and 'downgrade' - however, the reality is much more nuanced.

How is Atour benefiting from Downgrading?

As we discussed earlier, there are 5 different ‘categories’ of hotels and corresponding customer groups. In context of the slowing economic growth and exacerbated pressures on various ‘groups’ (specifically professional services like consultants/bankers) - travel budgets have been cut by many professional organizations. Ask your sell side broker in China - and they will likely tell you that their budgets used to allow them to stay at 5 Star Hotels (Ritz Carlton at Shanghai IFC, Four Seasons at Shenzhen Futian etc) but now can only allow them to stay at Atour or Ji.

Atour has seen significant growth of its corporate business from this dynamic - with some of its corporate customers growing 3x in the past year. So yes, in this context, the customers are downgrading, and Atour is benefiting from this trend - corporate customers are reducing spend while mitigating the impact on experience (other than brag-ability on dating apps, no major experiences are sacrificed).

How is Atour benefiting from Upgrading?

Travel is one of those categories where leisure consumers are still upgrading — representing one of the only consumer categories where growth has rebounded — with higher RevPar across the industry over past years (see below). The closure of independent hotels and increase in adoption of chained hotels is indicative of consumers’ willingness to pay more for a superior experience. This data is corroborated by reasonably strong travel data from Dragon Boat Festival last week. Furthermore, with Atour’s membership program - the business travelers who use Atour (over Bonvoy) will likely adopt Atour for their personal travels, especially as the company’s hotel footprint continues to expand.

Superior financial performance

Atour's advantages discussed has resulted in superior business economics over competitors.

RevPAR:

As shown below, Atour generates higher RevPAR (Revenue per available room) than peers. RevPAR has surpassed pre-Covid levels.

Atour has maintained a high occupancy. Notably, it does so without offering discounts. You can see for yourself — when booking rooms on OTAs you will find that Atour is almost never on discount. This is a testament to its differentiated service quality and customer loyalty.

While H-World has done a good job keeping occupancy high, this is largely due to reliance on midscale hotels with a different operating model.

Growth:

Atour has grown its room count at a much faster CAGR compared to its peers. While there is a base effect to consider, the fact that Atour tripled its room count even throughout Covid demonstrates strong demand for the brand.

Atour’s occupancy rates (previous chart) are even more impressive in light of the rapid expansion, as new properties generally have ramp-up periods that bring down average occupancy rates.

P&L:

Atour also leads its peers in revenue and profit CAGR. Notably, Atour is the only one among its peers to have maintained positive profits throughout the pandemic (driven by significantly lower proportion of leased hotels vs. the listed peers).

During all of 2022, Atour only had four hotel closed down.

Valuation

The value drivers of Atour are simple.

Hotel revenue: Rooms Available x Occupancy Ratio x Average Daily Rate x Royalty Rate

The key assumptions are:

Rooms available:

We’ll use management guidance of 2,000 hotels by 2025 (currently at 1302 hotels + 674 in the development pipeline, meaning the 2,000 target is very much achievable), which should be approximately 230k rooms (this compares to H-World currently at 9,817 hotels and 955k rooms).

Atour is in ~200 cities, mostly tiers 1/2, while H-World is present in 1,290 cities (and targeting 2,000). There is much more room to grow beyond 2025.

Note that chain hotel penetration is still relatively low in China (32% vs. 72% in the US as of 2020).

Occupancy:

Likely to be stable to down vs. 2023, given the ‘reopening revenge travel’ and constrained supply in 2023; ~70-80% (midpoint around 75%) is likely reasonable.

Average daily rate:

In addition to the core Atour brand (upper-midscale) the company also operates Atour S (upscale) and Atour Light or “Qingju” (mid-scale).

The success of Atour Light is a significant element of the company’s growth strategy through 2030, given the need to expand into lower tier cities.

While Atour Light has a lower ADR, it is not by much (in 2023, ADRs were RMB 450, 618 and 430 respectively for Atour, S, and Light). We will therefore assume that blended ADR remains flat (~ RMB 450).

Royalty rate:

Franchisees are paying 7-9% royalties (includes both royalties and central booking fees through Atour channels).

Given Atour’s strong RevPAR leading to high franchisee profitability/payback, we believe Atour should be able to generate higher ‘take’ over time through higher direct channel bookings (Atour at ~80% vs. 90%+ at H-World)

With these assumptions, we derive a royalty revenue of approximately 2bn RMB.

Atour’s total revenue would be much higher than this, because it also includes items like other revenue received from franchisees (to cover hotel manager/HR manager payroll and room supplies), leased/owned hotel operations, and the retail business. But the margin for these would be much lower.

We’ll let you decide what this capital light cash flow stream should trade at. Let’s say at 70% margin, this is RMB 2bn * 0.7 = 1.4 bn or approximately US$200 mn. At a market cap of $2.4 bn, Atour is trading at 12x 2026E earnings.

We are ignoring US$500 mn of net cash and short term investments on the balance sheet, as well as the longer term growth opportunities in Atour Light (“Qingju”), which means the ceiling of hotel openings in the future is not just limited to 2,000 hotels. In addition, we also treat the retail business as optionality, which reached run-rate GMV of RMB 2bn having grown 277% in the most recent quarter. Last year, management noted that the GPM of the retail business was 40%, with net income breaking even. That was when GMV was 1/3rd of today’s level, which means today retail business is certainly profit-making today.

What are the risks?

Increased competitive intensity in the upper-midscale category

H-World has made it clear that they would like to enter this category - as it doesn’t take a genius to recognize the opportunity in this segment. This risk is somewhat mitigated by the fact that H-World has more brands than you can count on a hand in this category - they compete internally for resources and H-World itself has had a culture of focusing on efficiencies (as opposed to services). Suffice to say it will take them some time (as H-World admitted openly on its conference call).

Service dilution as the company expands.

As we’ve discussed, Atour’s key success factor thus far has been the result of it’s differentiated service offering. As the company expands, it is imperative for the company to maintain its service-oriented culture and maintain its ‘soft product’ offering to constantly ‘wow’ customers. Additionally, the company is also fighting against adaptive preferences. (I.E. You will be extremely impressed the first time you ride a HSR Train in China, less so the 15th time.) This is something to be tracked.

Will Atour age gracefully?

Looking at the history of hotel openings, ATAT really ramped up store openings in the recent years, so over time it is important to assess how Atour hotels perform after they’ve aged. Arguably, ATAT customers come to stay due to the soft product, but the hard product cannot lag too much. The company will need to work with franchisees to “refresh” the hard product as they reach that 5-7 year vintage to ensure that the hard product remains competitive.

Shareholder returns

Given its capital-light business model and strong cash position, we believe Atour has a high capacity for returning capital to shareholders.

Management has expressed intention to pay dividends this year, and they can be more aggressive in returning capital to shareholders now, especially that Legend Capital has substantially completed its liquidation (with liquidity being less of a constraint for conducting share repurchases).

Disclosure: The author(s) have a long position in Atour

Thank you for reading — If you found this post helpful, I would really appreciate a subscription or a share! :)

I linked to this and your other piece in my Emerging Market Links + The Week Ahead (June 17, 2024): https://emergingmarketskeptic.substack.com/p/emerging-markets-week-june-17-2024

I stayed at the Hanting Hotel Changchun Train Station Branch (I think part of H World Group (NASDAQ: HTHT)) maybe several years ago as there were no international hostels there. As I noted last year, there was a little surprise when I came back: (https://emergingmarketskeptic.substack.com/p/em-fund-stock-picks-commentary-august-8-2023):

"Also, I had to stay in a hotel in Changchun (sort of a local chain version of a Holiday Inn Express that local tourists or business travelers would stay at - not international business travelers with fat expense accounts) as there were no hostels there. The room was up to international standards regarding cleanliness and comfort. However, and when I came back after walking around the city for two hours after checking in, I was greeted by these “room service” calling cards shoved under my doorway:"

https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F2a94ea2f-7862-4b8f-ba08-1a7b844b89f0_880x662.png 🤣🤣🤣

[At least they didn't come to my door in person to offer any services and I never answer the phone at a Chinese hotel... normally go for international hostels or guesthouses where this sort of extra service is not available.....]

Excellent write-up! Thanks!